The Death of the Wallet: How Many Americans Have Stopped Carrying Physical Cards

Tap-to-pay used to feel like a novelty. For a lot of people, it's now just the default. Oobit surveyed 1,000 U.S. adults to find out how often they leave home wallet-free, where physical cards still win, and what it would take to start paying with crypto the way they already pay with everything else.

Key Takeaways

- 1 in 4 American adults (25%) leave their wallet at home either deliberately or without thinking, including just over 1 in 10 (11%) who say they no longer feel they need it.

- More than 2 in 5 Gen Z Americans (41%) treat their phone or smartwatch as their primary payment method, compared to 1 in 4 American adults nationally (25%).

- Over 1 in 4 American adults (28%) have walked away from a purchase because the merchant didn't accept tap-to-pay, and over 2 in 5 (44%) say a no-tap business feels outdated.

- Nearly 1 in 2 American adults (49%) say losing their phone would be worse than losing their wallet, and more than 1 in 3 (35%) expect the physical wallet to be obsolete or mostly replaced within 5 years.

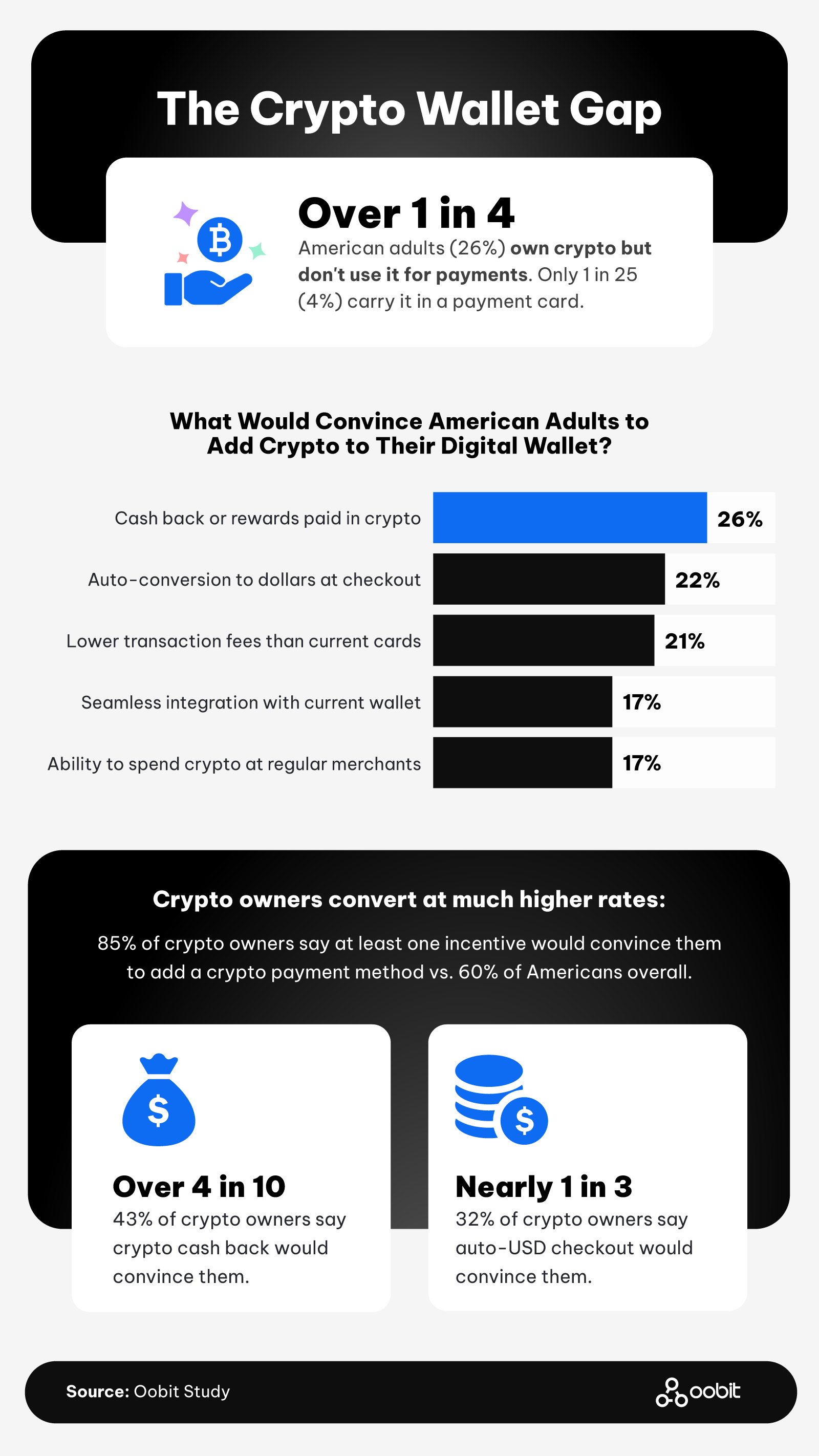

- Over 1 in 4 American adults (26%) own cryptocurrency but don't carry it in a payment card, and more than 4 in 5 American crypto owners (85%) say at least one incentive would convince them to add a crypto-funded payment method.

- More than 1 in 6 American adults (17%) have memorized their full credit card number, and roughly 1 in 4 of those (25%) say it has caused them to spend more.

How the Wallet Became Optional

The shift away from physical cards isn't uniform. It's a generational story, and Gen Z is at the front.

Phones Are Doing the Work

- Phone or smartwatch as primary payment method, by generation: more than 2 in 5 Gen Z (41%), more than 1 in 4 millennials (26%), nearly 1 in 6 Gen X (17%), and roughly 1 in 12 baby boomers (8%). The national average was 1 in 4 American adults (25%).

- More than half of American adults (56%) used phone tap-to-pay in the past 30 days, and nearly 3 in 5 (58%) used either a phone or smartwatch tap.

- Nearly 1 in 4 American adults (24%) left home carrying only their phone on 5 or more days in the past month, and more than 1 in 6 (17%) on 10 or more days.

Leaving the Wallet Behind

- The relationship American adults have with the physical wallet has broken down four ways:

- 47% never leave home without it.

- 28% only leave it at home by accident.

- 14% leave it without thinking about it.

- 11% leave it deliberately because they no longer need it.

- Average days per month going wallet-free, by generation: 6 days for Gen Z, 4 for millennials, 3 for Gen X, and 1 for baby boomers.

- More than half of Gen Z (54%) and nearly half of millennials (45%) had gone wallet-free at least one day in the past month. Among older Americans, that figure dropped to more than 1 in 4 Gen X (27%) and just over 1 in 7 baby boomers (15%).

When Tap-to-Pay Isn't There

- Nearly 2 in 5 American adults (38%) had walked away from a non-tap merchant or come close to walking away. Gen Z was more than twice as likely as baby boomers to do so (36% vs. 14%).

- More than 1 in 3 American adults (37%) say carrying physical cash feels old-fashioned.

The Wallet's 5-Year Outlook

- Looking 5 years out, expectations split sharply. More than 2 in 5 American adults (42%) expected the wallet to remain common but used less often, more than 1 in 4 (28%) expected it to be mostly replaced with cards as backup only, 1 in 5 (21%) expected things to stay about the same, roughly 1 in 14 (7%) expected the wallet to go fully obsolete, and just 1% expected it to become more essential than today.

- Among American adults who used phone tap-to-pay in the past 30 days, more than 2 in 5 (44%) expected the wallet to be obsolete or mostly replaced within 5 years. The national figure was roughly 1 in 3 (35%).

The Card Itself Is Fading

- More than 1 in 6 American adults (17%) had memorized their full credit card number. Another 1 in 9 (11%) knew most of it, and just over half (52%) had memorized at least part of their number.

- Memorization peaked among Gen X (19%) and millennials (19%), compared to Gen Z (12%) and baby boomers (9%).

- 1 in 4 American adults who had memorized their card (25%) say it causes them to spend more, and nearly 1 in 12 (8%) say it causes them to spend significantly more.

The Gap Between Owning Crypto and Spending It

Crypto ownership isn't fringe anymore. The gap is what owners actually do with what they hold.

Who Owns Crypto and Who Spends It

- Nearly half of American adults (46%) had owned cryptocurrency at some point, and another 1 in 10 (10%) say they are interested but have never owned it.

- Crypto ownership ran higher among older generations than tap-to-pay habits did: nearly 1 in 3 Gen X (32%) and nearly 1 in 3 millennials (31%) owned crypto, compared to 1 in 4 Gen Z (25%) and roughly 1 in 6 baby boomers (16%).

- Just over 1 in 10 American adults (12%) had ever paid with crypto at an in-store checkout, whether through a card or directly.

Why the Crypto Card Hasn't Caught On

- Nearly 9 in 10 American crypto owners (89%) didn't use a crypto-funded payment card.

- Roughly 1 in 8 American adults (13%) say they have considered a crypto-funded payment card but haven't adopted one, on top of the 1 in 25 (4%) who currently used one.

Comfort With Crypto in the Wallet

- More than 1 in 3 American adults (35%) are comfortable with cashback paid in crypto, 30% with a crypto-funded debit card, 27% with tap-to-pay using crypto from a phone, 26% with a stablecoin balance, and 24% with a Bitcoin-backed payment method.

- Among American adults whose primary payment method was already a phone or smartwatch, comfort with crypto-in-wallet features ran 9 to 16 percentage points higher than the national average. The biggest gap was on tap-to-pay using crypto from a phone (43% vs. 27% nationally).

What Would Bridge the Gap

- The top incentives that would convince American adults to add crypto to their digital wallet are cashback or rewards paid in crypto (26%), auto-conversion to dollars at checkout (22%), lower transaction fees than current cards (21%), seamless integration with their current wallet (17%), and the ability to spend crypto at regular merchants (17%).

- 40% of American adults say no incentive would convince them to add a crypto-funded payment method. Among American crypto owners, that figure drops to 15%.

Where Payment Goes From Here

The data points to a lopsided shift. Tap-to-pay has gone mainstream, especially among younger Americans, but most crypto owners haven't connected what they hold to how they actually pay. The incentives people say would change that look a lot like what already keeps them loyal to their current rewards cards: cashback, easier dollar conversion, and lower fees—and understanding the settlement flow is what makes crypto spending feel as seamless as a normal card swipe. The Americans most open to using crypto in their wallet are the ones already paying with their phones.

"The wallet isn't disappearing because someone designed it that way. It's because the phone has gotten good enough. Crypto is in a similar spot now. The infrastructure exists. The job left is making it feel like everything else people already do at checkout."

— Amram Adar, CEO, Oobit

Methodology

Oobit surveyed 1,000 American adults about their payment habits, attitudes toward the physical wallet, cryptocurrency ownership, and views on crypto-funded payment methods. The survey was conducted via CloudResearch Connect. Respondents were 51% women and 49% men. Generational breakdown was 50% millennials, 23% Gen X, 17% Gen Z, and 9% baby boomers. Respondents had incomes ranging from under $25K (22%), $25K+ to $50K (23%), $50K+ to $100K (37%), $100K+ to $150K (12%), and $150K+ (6%), with a median of $50K. The margin of error is ±3.1% at a 95% confidence level.

About Oobit

Oobit is a crypto payments platform that lets users tap and pay with digital assets directly from their phone, no physical card required. Using NFC technology, Oobit converts crypto to local currency at the point of sale, so users can spend Bitcoin, USDT, and other digital assets anywhere Visa or Mastercard is accepted.

Fair Use Statement

The information in this article may be used for noncommercial purposes only. If shared, proper attribution with a link to Oobit must be included.