Most Americans don't fire their bank. They just start using it less. A paycheck still lands there, but friends get paid back through a wallet app. The savings account stays open, but money for online purchases sits somewhere else. The bank isn't replaced, it's unbundled, one task at a time.

Oobit surveyed 1,002 Americans about how they use crypto wallets alongside or instead of their banks for everyday financial tasks. The results show banks losing ground in specific places, holding it firmly in others, and a generation of users who already mix both without thinking twice.

The tasks leaving the bank aren't random. Americans who use crypto wallets are picking specific jobs, usually the ones banks make slow, expensive, or awkward, and handing them to crypto.

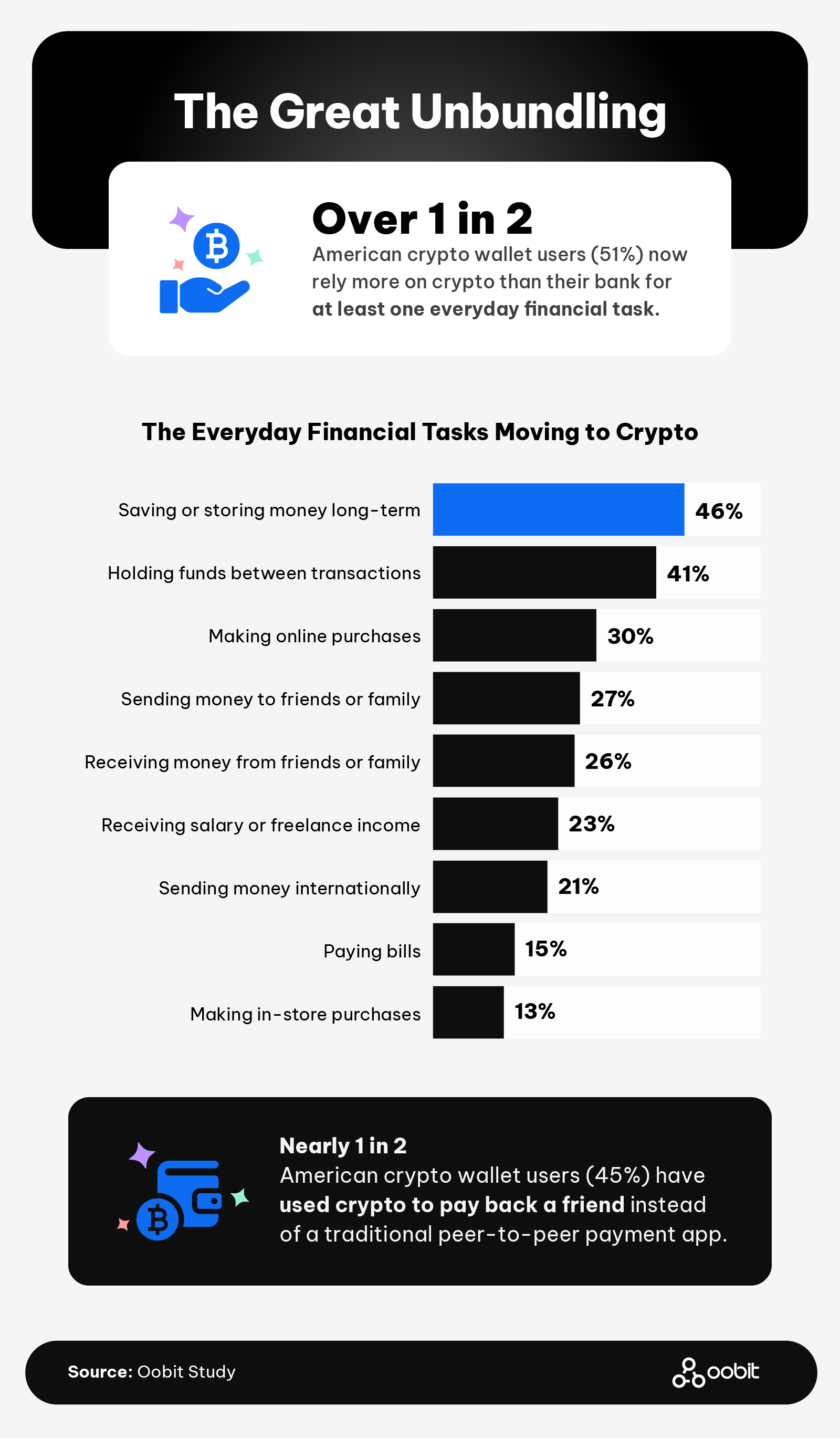

Among American crypto wallet users, the tasks most likely to move to crypto are:

The top two slots go to storage-type tasks, which directly challenge the most basic thing a bank does: holding your money.

International transfers are where the gap between banks and crypto gets largest, in crypto's favor. Among crypto wallet users who send money across borders, nearly 1 in 2 (46%) rely more on crypto than their bank for that task. Compare that to 35% for person-to-person payments and 20% for online purchases, and international transfers look like the sharpest edge of the shift.

Peer-to-peer behavior tells a generational story. Nearly half of American crypto wallet users (45%) have paid back a friend in crypto rather than using a traditional peer-to-peer payment app. Among Gen Z, that number jumps to 55%, 10 points higher than millennials and the highest rate of any generation.

Over 1 in 2 American crypto wallet users (51%) now rely more on crypto than their bank, or have fully replaced their bank, for at least one everyday financial task. The other 49% either split their usage evenly or still lean on their bank for most things.

While 16% of American crypto wallet users have fully replaced their bank for at least one everyday task, full replacement is rarer. Paycheck routing, not peer-to-peer or shopping, is where the bank is getting cut out cleanly.

People don't move financial tasks to crypto for one reason. But the top reason isn't what you might guess.

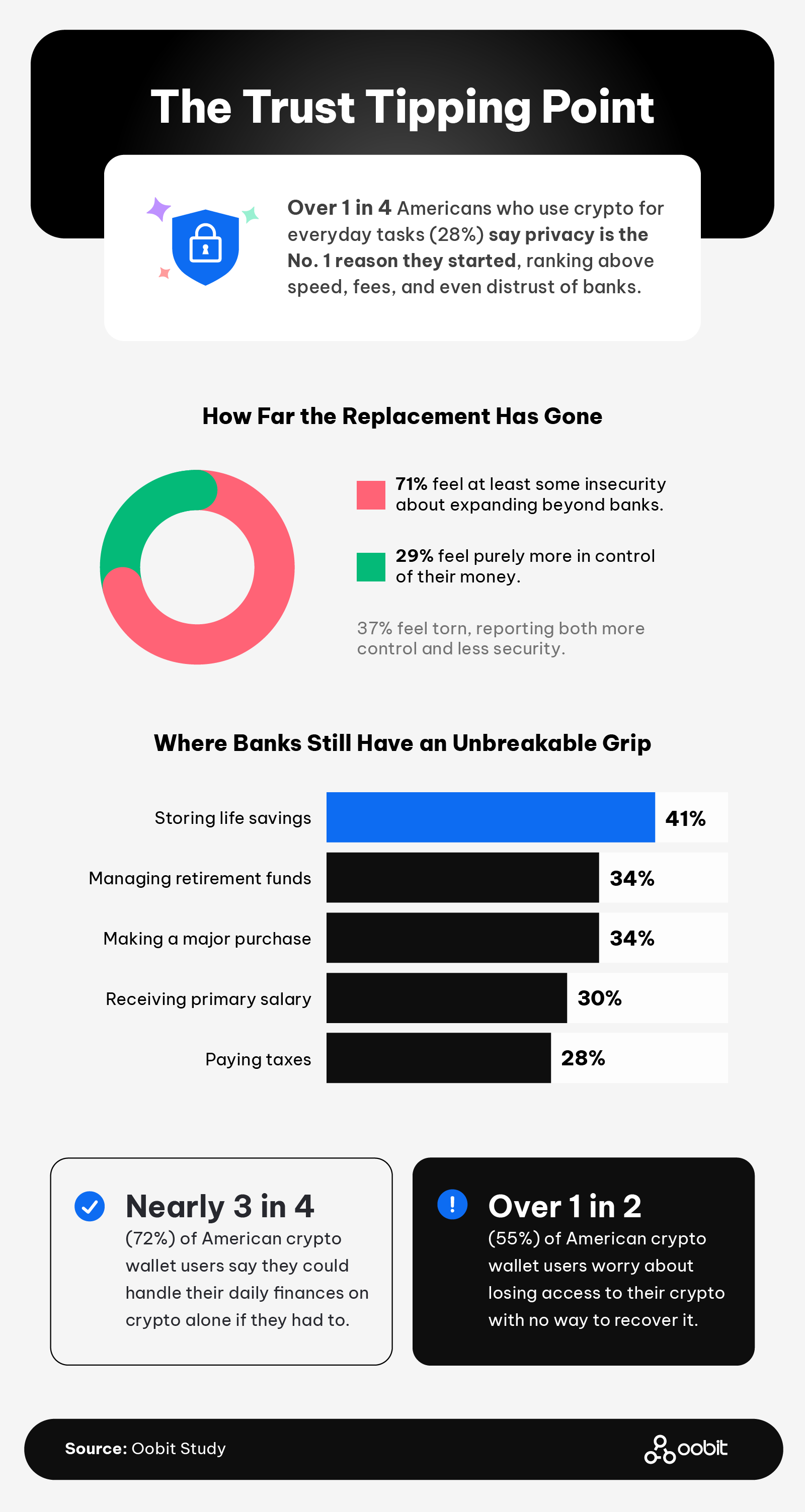

Over 1 in 4 Americans who use crypto for everyday tasks (28%) said privacy is the No. 1 reason they started. That ranks above speed (22%), lower fees (12%), and distrust of banks (15%). Among American men who use crypto wallets, privacy was still the top motivator, cited by 31%. But women most often started using crypto because they believe it's the future of finance (29%).

Nearly 3 in 4 American crypto wallet users (71%) feel at least some insecurity about expanding their finances beyond their bank. Another 37% are torn, feeling more in control of their money while also feeling it's less secure. Only 29% feel completely more in control. Overall, 54% of wallet users said crypto has made them feel more financially independent.

Comfort with crypto builds with use. Over 1 in 3 regular American crypto users (37%) said they could handle everyday finances solely in crypto without major disruptions, compared to only 17% of occasional users. And nearly 3 in 4 crypto wallet users overall (72%) said they could manage their daily finances on crypto alone if they had to.

One specific task lines up with the biggest trust jump. Nearly 2 in 3 Gen Z Americans who use crypto wallets (66%) trust crypto more than their bank for moving money quickly. That's 16 points above millennials (50%) and the highest rate of any generation.

Some tasks still live mainly at the bank for now.

Over 2 in 5 American crypto wallet users (41%) said they would never trust crypto to store their life savings. That's the single biggest holdout for traditional banks. The full list of tasks Americans still trust banks with most:

A pattern runs through all five: they're high-stakes, low-frequency, or both. The stakes shift with the amount of money involved, and recovery matters more the bigger the balance. Over 1 in 2 American crypto wallet users (55%) worry about losing access to their crypto with no way to recover it, which helps explain why those specific tasks are slower to move.

Barriers to further adoption break down by generation:

And among curious non-owners (people who know about crypto but don't use it), 32% said nothing would change their mind about using crypto. Among regular crypto users, only 5% said the same. The more people actually use crypto, the less likely their positions are to stay fixed.

What's actually happening isn't a full unbundling, but a splitting. American crypto wallet users aren't walking away from their banks all at once. Instead, they're moving everyday tasks to crypto first, usually transfers and peer-to-peer payments.

The tasks still living at the bank are the ones people do rarely or treat as high-stakes. What's moving first is the day-to-day money, and that's where habit change actually starts.

Oobit surveyed 1,002 Americans about their cryptocurrency use and everyday financial habits, including which financial tasks they use crypto wallets for, how far they have replaced traditional banks, what drives or prevents adoption, and what conditions would move them toward crypto. The survey was conducted via CloudResearch Connect. Respondents were 46% men, 52% women, and 2% non-binary. Generational breakdown was 52% millennials, 24% Gen X, 16% Gen Z, and 8% baby boomers.

Of the full sample, 17% reported active use of crypto wallets and answered detailed questions about specific financial tasks, replacement behavior, and trust. As with all survey data, responses are self-reported and may be subject to recall or social desirability bias. Percentages that do not total 100% are due to rounding.

Oobit is a crypto payments platform that enables users to spend digital assets in the real world wherever major cards are accepted. By bridging crypto and everyday commerce, Oobit makes digital currency practical and accessible for daily use.

The information in this article may be used for noncommercial purposes only. If shared, proper attribution with a link to Oobit must be included.