Cryptocurrency has moved from trading screens to spending apps, but the bigger shift may be happening at the bank itself. As bank stocks slide and economic uncertainty grows, younger Americans are rethinking where they keep their money, and many are already moving it.

To understand how deep this goes, Oobit surveyed 1,004 Americans ages 18 to 34 about their banking habits, trust in financial institutions, and attitudes toward crypto and stablecoin alternatives. We also analyzed 22,118 Reddit posts across 16 subreddits to track how the conversation is shifting in real time.

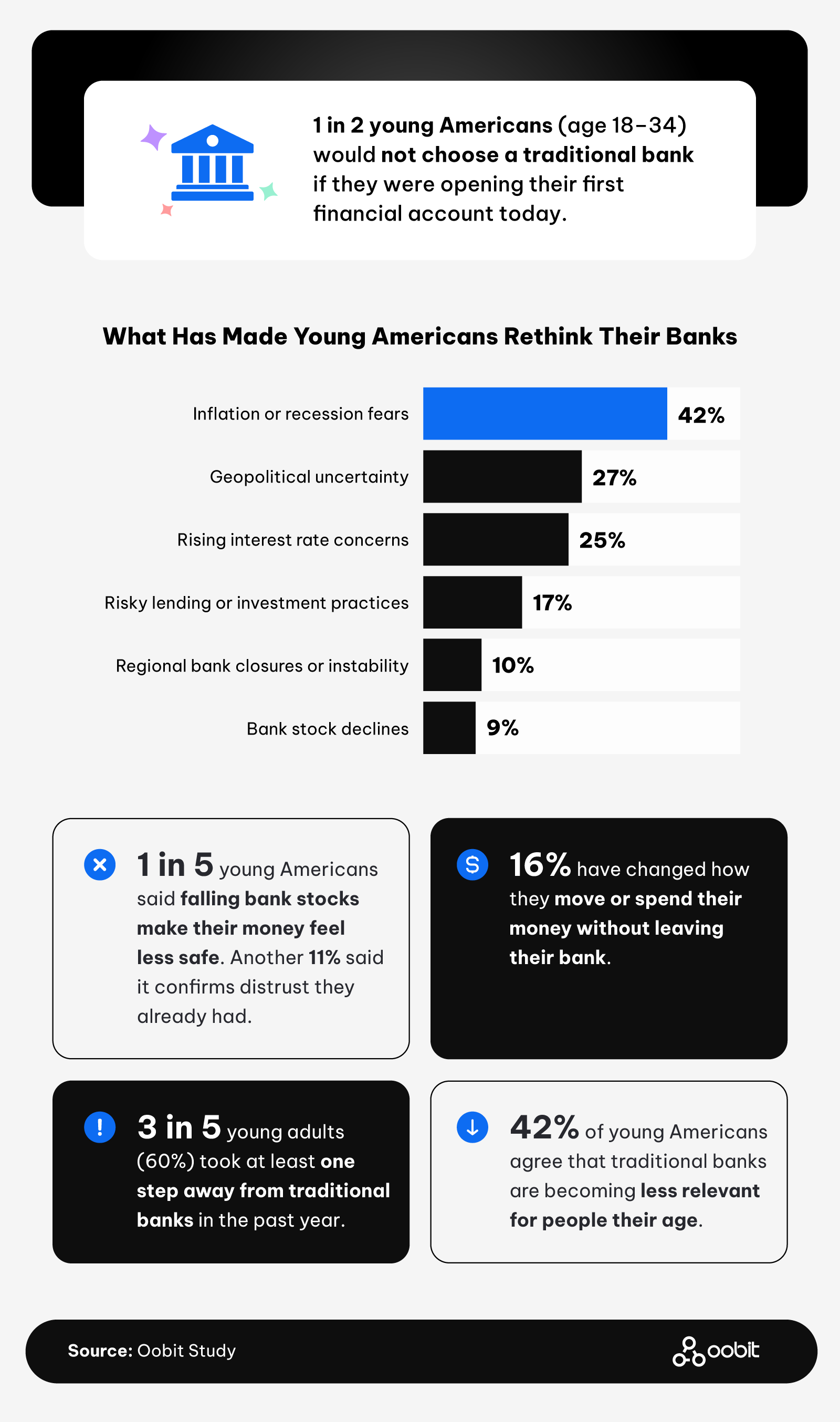

If given a clean slate, half of young Americans wouldn't walk into a traditional bank. And the generational breakdown adds a wrinkle.

Over 1 in 2 millennials (53%) would skip a traditional bank if starting from scratch, compared to nearly 1 in 2 Gen Z respondents (45%). Millennials are also more likely to juggle 3 or more financial platforms (32% vs. 27%), suggesting the pull away from banks gets stronger with age and experience.

But here's the catch. Even among those who say they'd skip traditional banks, the majority still rely on them. Over 1 in 2 young Americans (55%) still trust a bank most for storing savings, and nearly 3 in 5 (59%) still trust a bank most for receiving a paycheck.

When asked what made them rethink their banks, inflation or recession fears topped the list at 42%, followed by:

The actions are already matching the attitudes. Over 3 in 5 young Americans (62%) took at least one step to move money away from a traditional bank in the past year. Another 20% said falling bank stocks make their money feel less safe, while 11% said the declines just confirm the distrust they already feel.

Income tells an interesting story, too. Over 2 in 5 young Americans earning under $50K (40%) didn't even know bank stocks were falling, compared to nearly 1 in 4 of those earning $50K or more (24%). Yet, over 1 in 2 lower-earning young Americans (56%) still took at least one step away. Among those earning $100K or more, that number climbs to 75%.

Credit unions are also attracting attention. Over 1 in 4 young Americans (26%) would choose a credit union first if starting fresh, making it the second most popular choice overall after a traditional bank. Credit unions are also the top alternative for millennials (28%) and those earning $50K to $74K (33%). Fintech apps, despite being used by 44% of young Americans today, rank fourth as a first choice at just 4%, suggesting they serve as spending tools, not financial foundations.

Meanwhile, 2 in 5 young Americans (42%) agree that traditional banks are becoming less relevant for people their age. And 16% have already changed how they move or spend their money without closing their accounts. The behavior is shifting before the accounts do.

Bank distrust isn't only pushing young Americans toward fintech apps and credit unions. For a growing share, crypto is part of the answer, though spending it is still a problem.

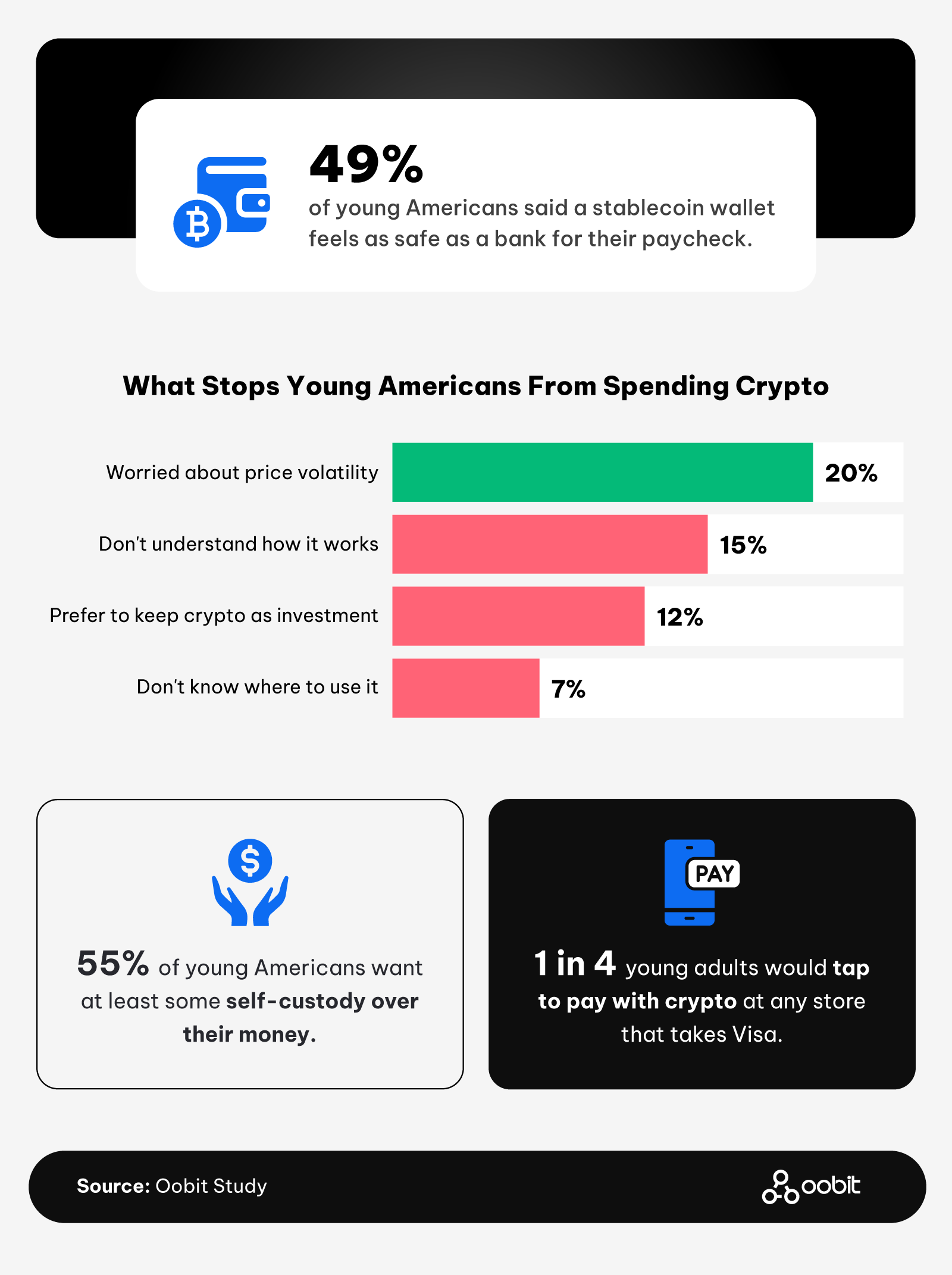

Nearly 1 in 2 young Americans (49%) say a stablecoin wallet feels as safe as a bank for holding their paycheck. And 55% want at least some self-custody of their money, meaning they want to personally control at least part of their money rather than leaving it all with a bank or platform.

Stablecoin awareness splits sharply by income. Nearly 2 in 3 young Americans earning $100K or more (66%) have heard of stablecoins, compared to 41% of those earning under $50K, the widest demographic gap on stablecoin awareness in the study.

The appetite for self-custody is actually stronger among lower earners. Young Americans earning under $50K are more likely to want self-custody (17%) and less likely to want bank-only control (33%) than those earning $50K or more (13% and 43%). The people least served by traditional banking are the ones most interested in financial independence from it.

That said, spending crypto is a different story. Over 4 in 5 young American crypto owners who have tried to spend it (83%) said it's still difficult to use for everyday purchases. The top barriers were:

Over 2 in 5 Gen Z respondents (44%) said they have no interest in spending crypto at all, compared to over 1 in 3 millennials (35%). Among millennials who do cite a barrier, volatility concerns (22%) and investment preference (14%) rank highest. They're more engaged with crypto than Gen Z, but more cautious about spending it.

Still, 1 in 4 young adults would pay with crypto at any store that takes Visa. And when those open to crypto spending were asked what would get them there, the top motivators were consistent across income levels: transparent exchange rates, better education, and the ability to tap to pay at any store.

Nearly 1 in 2 young Americans earning $50K or more (46%) own cryptocurrency, compared to under 1 in 3 of those earning under $50K (29%). Ownership also varies by generation, with 41% of millennials and 32% of Gen Z reporting they own crypto.

Gen Z is more reactive to market signals, even though their crypto engagement is lower. One in 5 Gen Z respondents (20%) and 16% of millennials said they would move money into a digital wallet if bank stocks keep falling.

The survey data tells one side of the story. Reddit tells the other.

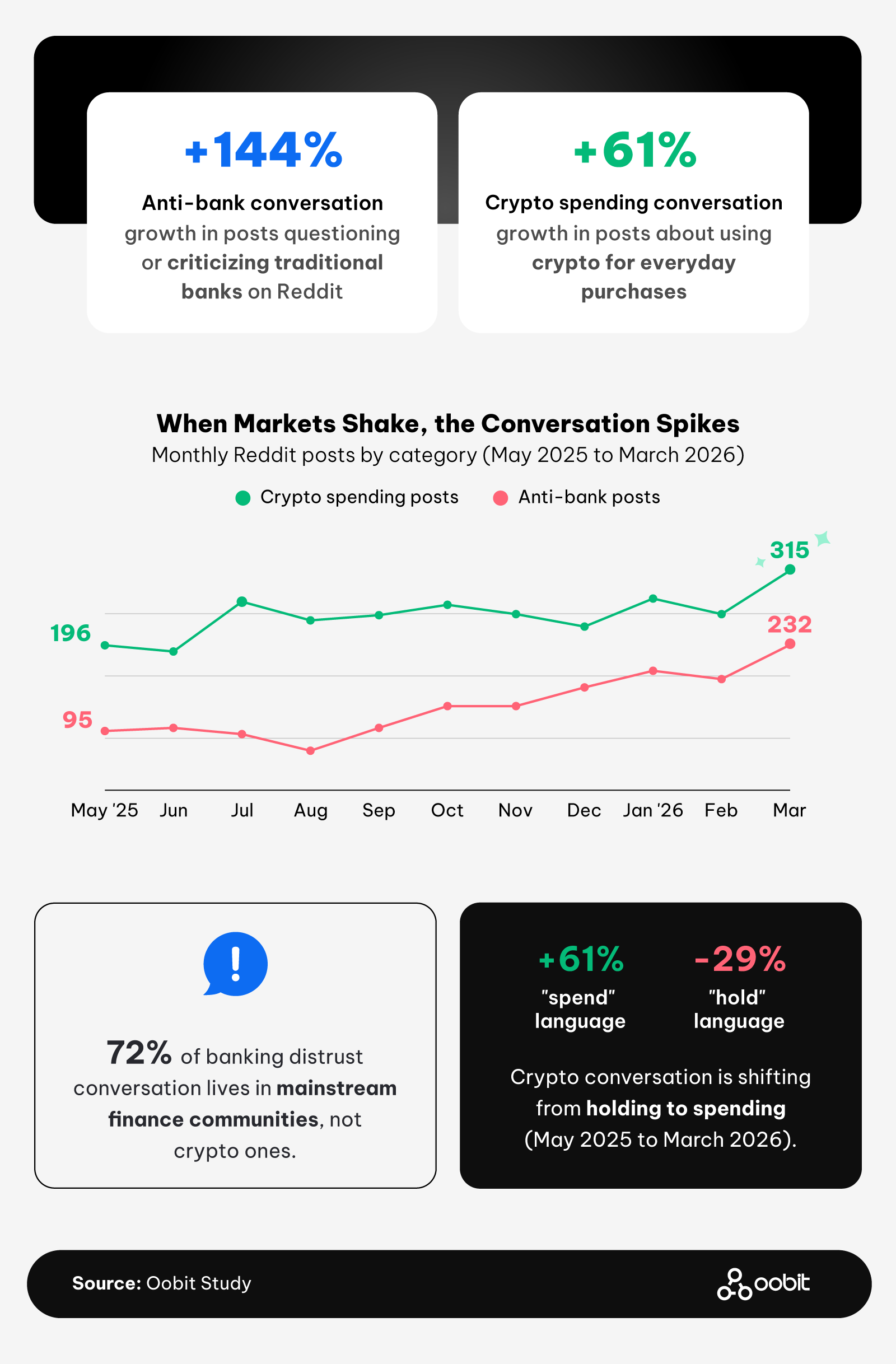

Anti-bank conversation on Reddit grew 144% from May 2025 to March 2026. Crypto spending conversation grew 61% over the same period. The distrust of banks isn't coming from where you'd expect: 72% of the anti-bank conversation lives in mainstream finance communities like r/personalfinance, r/banking, and r/povertyfinance, not in crypto subreddits.

The same pattern holds for discussions about neobanks, digital banks that operate without physical branches. Over 7 in 10 neobank-related posts (74%) appeared in mainstream finance communities, not crypto-native ones.

What's driving the conversation? Not rage against the system. Only 6% of the 22,118 posts analyzed were motivated by institutional distrust. General curiosity (52%) and excitement about spending crypto in real life (27%) accounted for nearly 4 in 5 posts in the dataset.

The highest-engagement anti-bank posts were directly tied to financial catalysts. A February 2026 post about Federal Reserve jobs data revisions scored 15,922 upvotes, and a March 2026 post comparing private credit to the 2008 crisis scored 2,149.

There's also a language shift happening inside crypto communities. In June 2025, "spend" language outpaced "hold" language in crypto-native subreddits for the first time in the 12-month tracking period (50.1% spend share). Spend share has since stabilized between 30% and 42%, up from 4% in April 2025. At the same time, "hold" language declined 29% across the full period. The conversation is moving from accumulation toward use.

Where people hang out online tracks with how they think about crypto. r/defi had the highest spend-to-hold language ratio of any crypto-native community (64% spend share), while r/wallstreetbets sat at just 11%. The communities closest to decentralized finance infrastructure talk about spending. The trading communities still talk about holding.

Young Americans aren't storming out of banks. Most still deposit their paychecks and park their savings in one. But the relationship is thinning. More than half would choose something else if they could start over, and a majority already took at least one step away in the past year.

The gap right now is usability. About half of young Americans see a stablecoin wallet as safe enough for a paycheck, but many of those who've tried to spend crypto say it's still hard. Tools that close that gap, ones that make it easy to hold, convert, and spend digital assets in everyday life, are what can turn shifting sentiment into actual behavior change.

Banks aren't going to disappear overnight. But the generation that's supposed to fill their deposit base is already looking elsewhere.

Oobit surveyed 1,004 U.S. adults aged 18 to 34 in 2026 via the CloudResearch Connect platform about their banking habits, trust in financial platforms, and attitudes toward cryptocurrency and stablecoin alternatives. Respondents were asked about current money management tools, platform trust for specific financial tasks, actions taken in the past 12 months, the influence of recent financial events, social media's role in financial decisions, stablecoin and crypto experience, barriers to crypto spending, and attitudes about the future of banking. The gender breakdown was 55% women, 40% men, and 3% non-binary. Generationally, the sample consisted of 63% millennials and 37% Gen Z.

Separately, Oobit analyzed 22,118 Reddit posts across 16 subreddits from April 2025 to April 2026, sourced via the Pullpush API and Arctic Shift Archive. Posts were categorized into four keyword groups: anti-bank language, neobank language, crypto spend language, and crypto hold language. Communities were classified as mainstream (r/personalfinance, r/banking, r/povertyfinance, r/Fire, r/fintech, r/millennials, r/GenZ, r/CreditUnions) or crypto-native (r/bitcoin, r/cryptocurrency, r/wallstreetbets, r/CryptoMarkets, r/ethereum, r/defi, r/stablecoins). Sentiment was classified by driver: general curiosity, crypto spending excitement, news reaction, and institutional distrust.

Oobit is a crypto payments platform that lets users spend digital assets wherever major cards are accepted. Through the Oobit app and crypto card, users can connect their wallets and tap to pay in-store, online, or on the go, earning crypto cashback along the way and turning crypto into a practical tool for everyday spending.

You're welcome to share or reference this research for noncommercial purposes. Just credit Oobit and link back to us.